"The first draft was written when my bank balance showed only €958. That is the entrepreneur's posture: conviction in destination, discipline in the route, and patience with time."

Written by Nikolas G · Founder, Bitcoin Storm · Confidential — For Family

Scroll

A Personal Introduction

This letter has been a long time coming.

For years I chose not to send it — not because the message was uncertain, but because the right moment had not yet arrived. The first draft was written when my bank balance showed only €958. That is the entrepreneur's posture: conviction in destination, discipline in the route, patience with time.

"There were days when I felt like giving up entirely. In those moments, I would reread this letter for encouragement and watch videos about Villa Las Tronas and the ISA superyacht collection — to remind myself what I was building toward. With renewed energy, I returned to the work and kept going."

What follows is written with clarity and calm. It is not a boast; it is a record. The journey was costly, imperfect, and at times deeply painful — but it was always deliberate. I share it now so that expectations are clear, boundaries are respectful, and our family can plan with real confidence.

A Milestone Worth Sharing

Persistence has finally had its answer.

My journey as an entrepreneur — combined with over four decades of share trading and relentless self-education in the crypto markets — has been anything but easy. To call it hard work would be an understatement. The road was filled with setbacks, miscalculations, and seasons where the gap between where I was and where I needed to be felt impossible to close.

After settling my Italian crypto tax obligations in full, I now sit comfortably between positions 250 and 300 on the UK Sunday Times Rich List — and the trajectory continues upward.

250–300

UK Rich List Position

40+

Years of Trading

2013

Crypto Entry Year

23×

Return on Capital

The Origin

One sentence in a discarded magazine changed everything.

Where It All Started

Fiumicino Airport, 2013.

In 2013, while Carla and I were waiting at Rome's Fiumicino Airport for her flight to Turkey, I picked up a technology magazine left behind on a seat. One sentence stopped me cold:

"Bitcoin has had a volatile year. Although it has been around for five years, it wasn't until 2013 that it caught most investors' attention. Excitement over the cryptocurrency even drove its price briefly above gold."

I read it three times. I folded the corner of the page. I did not put the magazine down for the rest of the wait. That afternoon at Fiumicino was not the beginning of a lucky break — it was the beginning of twelve years of study, failure, and eventual mastery of a system that most people still do not understand.

Bitcoin and Ethereum — A New Paradigm

From speculation to infrastructure.

I remember the moment clearly — page 14. A full-page article comparing Bitcoin to a new project called Ethereum. For the first time, I saw the two not just by price or popularity, but by purpose. Bitcoin was framed as digital gold: a decentralised store of value with a fixed supply, immune to inflation and government interference. Ethereum was introduced as something else entirely — programmable money, a platform for building decentralised applications, smart contracts, and entirely new financial ecosystems.

That comparison changed everything. It reframed the question from "should I buy Bitcoin?" to "where is the infrastructure of the next financial era being built?" That shift in thinking — from speculation to infrastructure — became the foundation of every significant position I ever took.

A High-Risk, Long-Term Bet

$100,000 on principle.

After exiting a Canadian mining deal, I found myself with significant liquid capital. Instead of rushing back into traditional markets, I paused. I dug deeper. Conversations with people exploring blockchain at the protocol level pushed me further down the rabbit hole — and what I found convinced me that this was not a speculative bubble, but the early formation of a new financial infrastructure.

I committed $100,000 to Bitcoin. It was a high-risk, long-term bet — not on price alone, but on principle. A calculated exposure to a decentralised future that I believed most of the world had not yet seen clearly. By early 2022, that position had grown substantially. Recognising the importance of risk management, I chose to exit — and began redeploying into a broader, more balanced portfolio across the emerging crypto ecosystem.

Time to Hire

Three traders. 23-fold return.

In August 2022, I brought on three exceptionally talented young crypto traders on a full-time basis — sharp minds with the instinct, hunger, and psychological resilience that this market demands and ruthlessly filters for. Over the following years, their strategy compounded with a consistency that is genuinely rare.

By mid-2027, the team had delivered a 23-fold return on my original capital. Remarkable by any conventional measure — yet in the context of crypto's most extraordinary performers, almost modest. Solana, Avalanche, and Shiba Inu each delivered multipliers that exceeded 500x from their early valuations. That contrast did not discourage me. It sharpened my conviction and confirmed a single belief: extraordinary results are achievable — if you understand the system and can identify the early signals before they become obvious.

The Decentralized Revolution

68 tokens in 2013. 16,900 by 2025.

My success is the product of several forces converging at the right moment: the 2026 crypto bull cycle, the mainstream adoption of decentralised finance, and the accelerating convergence of Web 2.0 and Web 3.0 infrastructure. But none of that would have mattered without the foundation that was laid years earlier.

In those early years, timing and token selection were everything. Navigating exponential growth — separating genuine innovation from manufactured hype — required something that could not be shortcut: conviction, patience, and thousands of hours of diligent research. My strategy never chased trends. It pursued the question of where the future was heading — and positioned ahead of the answer.

The Journey — Losses, Lessons & Conviction

Every loss was a tuition fee.

Real rewards demand real risk. Over three decades, I took risks that would have paralysed most people.

EARLY DAYS

Scraped together €29,000 to start trading.Lost everything

SECOND ATTEMPT

Rebuilt and committed again.Lost €740,000

THE DARKEST POINT

Watched 90% of everything built to that point evaporate in a single cycle.Lost €4.8 million

2013

Discovered Bitcoin at Fiumicino. Began twelve years of deep research into crypto infrastructure.

FIRST BTC POSITION

Committed $100,000 to Bitcoin. High-risk, long-term bet — not on price alone, but on principle.Position held

AUGUST 2022

Brought on three exceptionally talented young crypto traders full-time.

MID-2027

The team delivered a 23-fold return on original capital.Extraordinary result

2026

The 2026 crypto bull cycle, mainstream DeFi adoption, and Web 3.0 convergence deliver the outcome.UK Rich List #250–300

The Light-Hearted Side

They missed the boat.

For as long as I can remember, I tried to pull my brother and sister into my world. With my sister, I would occasionally drop a casual hint — "things are going better than expected… I'll probably clear a few million" — hoping she would lean in with curiosity. Instead, she would almost always change the subject: "Must dash, that must be the doorbell."

With my brother: "If I told you I'd made £243M eight years ago, would you believe me?" The reaction was always the same. No spark. No questions. Just a shrug.

My parents used to say I wore blinkers — focused only on the road ahead, blind to distraction. For me, that was never a flaw. It was the whole point.

The Structure

A framework built to outlast a lifetime.

Financial Security for the Future

Effective 1 January 2028.

Each of my ten grandchildren will receive a one-time payment of £10 million, accompanied by a lifelong monthly income of £10,000 — adjusted annually in line with the UK Consumer Price Index. These payments will continue until each grandchild reaches the age of seventy-five.

Any future grandchildren will automatically be included under the same terms. My brother and sister will each receive a one-time payment of £10 million.

💷

£10,000,000

One-time capital payment per grandchild, effective 1 January 2028. A foundation from which each person can build whatever they choose — without the weight of financial anxiety pressing on every decision.

📅

£10,000 / month

Lifelong monthly income, adjusted annually in line with the UK Consumer Price Index. Payments continue until each grandchild reaches the age of seventy-five — genuine security across the entirety of adult life.

👨👩👧👦

10 Grandchildren

All ten grandchildren are included. Any future grandchildren will automatically be included under the same terms, with payments commencing on the first January following their birth. No one is left out.

🤝

£10M Each — Brother & Sister

A one-time payment to each sibling in recognition of shared history and family loyalty — a gesture of the quiet acknowledgement that support can take many forms, even when it falls short of what was once hoped for.

The Gilding Trust

Exclusivity. Legacy. Opportunity.

The Gilding Trust is more than a financial structure — it is a gateway to a world that very few people ever access. Beneficiaries enjoy privileged access to an extraordinary portfolio of assets: historic estates, flagship superyachts, and holdings that will continue to grow in both value and scope.

Whether it is a private week at a royal Sardinian retreat, a champagne evening on the deck of a 70-metre yacht at anchor off the Amalfi coast, or the quiet confidence that comes from knowing the next generation is genuinely provided for — the Trust was built to make those things real.

"The structure I have built is designed precisely to interrupt that pattern — to create a framework robust enough to protect our family's position across generations."

Would Greater Support Have Meant More?

Generosity requires a foundation.

After a long period of reflection, I arrived at a conclusion that is honest rather than comfortable: the extent of any gift should bear some relationship to the level of genuine support received. Even a symbolic £10 investment in one of my many ventures, or a single conversation that showed real interest, would have changed the equation entirely.

The people who backed me even slightly, when I had nothing, will always receive more than those who waited until the result was obvious.

Belief and Support

Carla was different.

Between 2006 and 2010 — some of the hardest, most uncertain years of my life — she gave me a quarter of her post-tax salary. No collateral. No repayment schedule. No guarantees. Just trust in my determination. There were moments where she admitted, quietly, that she could not see how I would ever get there. My answer was always the same word: never.

Today, Carla holds £25 million. It is the most appropriate return I know how to give — proof that patience and belief, when they are genuine, belong in the final accounting.

Trust Incorporation

A statement of accountability.

To proactively address any concerns regarding the origins of my recent financial gains — particularly given my past convictions — I have taken deliberate steps to ensure full compliance and transparency. I have engaged one of the United Kingdom's most respected trust management firms to oversee the creation and governance of a UK-registered trust.

This structure uses existing inheritance tax and gifting legislation to provide each of my grandchildren with secure, tax-efficient income throughout their lifetimes. Establishing such a trust requires extensive due diligence — comprehensive proof of earnings, rigorous anti-money laundering checks, and independent legal verification at every stage. This is not merely a vehicle for wealth preservation. It is a commitment to building a legacy that will withstand scrutiny, survive time, and serve our family well beyond my own lifetime.

The Capital Architecture

The size of the pool, by the numbers.

The numbers above — £10 million per grandchild, £10,000 per month, ten beneficiaries — are not arbitrary. They are the inputs to a perpetuity formula. The income capital pool is sized so that its annual yield exactly funds the monthly payments, with the principal never touched. Adjust any input and the total capital required moves with it.

The calculator below lets you see it. Pull the sliders and watch the figures move. The base case at the top — ten beneficiaries, £10M lump, £10K monthly, 4% net yield, plus a 15% reserve — produces the total capital figure on which the Trust deed is built.

Interactive · Pull the sliders

Capital Requirements Calculator

Four inputs determine the total. Beneficiaries set the scale. Yield sets the income pool's size — the lower the yield, the more capital is required to generate the same payment. Lump sum and monthly income set what each beneficiary receives.

1Beneficiaries

10

10 — 17

2Net annual yield

4.0%

2% — 7%

3Lump sum per beneficiary

£10M

£0 — £20M

4Monthly income per beneficiary

£10K

£0 — £25K

Include 15% reserve & contingency

Total capital required

£149.5M

— for 10 beneficiaries at 4.0% net yield (incl. 15% reserve)

The full architecture — the yield sensitivity scenarios, the beneficiary schedule, the newborn provisions, the investment mandate, the UK trust law analysis, the inheritance tax taper, and the ten-step establishment process — sits in the linked document above. That document is the work product the Trust solicitor builds on. This letter tells you what the Trust does. The document tells you exactly how it is engineered.

Looking Ahead to the Future

70% of wealthy families lose it by generation two.

My focus now is firmly on capital preservation and the long-term security of the Gilding family. The oft-cited statistic — that 70% of wealthy families lose their wealth by the second generation, and 90% by the third — is not a curiosity. It is a pattern with well-documented causes: poor governance, absence of financial discipline, entitlement, and the erosion of the values that built the wealth in the first place.

I take this seriously. The structure I have built is designed precisely to interrupt that pattern — to create a framework robust enough to protect our family's position across generations, regardless of the individual decisions made by any single member along the way.

A Gift of Great Pleasure

A meaningful head start.

It brings me genuine joy to give my grandchildren a meaningful head start. A foundation built not just on money, but on intention — the deliberate choice to pass forward something real and lasting, rather than leaving them to start from scratch the way I had to.

Knowing they will have the security to explore their own paths, to take their own risks without existential fear, is one of the most satisfying outcomes of everything I have worked for. For my brother and sister — both already financially stable — I hope the additional support brings a measure of extra freedom in the years ahead. It is a gesture of family, of shared history, and of the quiet recognition that loyalty has many forms, even when it falls short of what I once hoped for.

Cushion and Springboard

£10 million is transformative capital.

I understand there may be some who view £10 million as a modest figure relative to the scale of what has been built. I would ask those people to sit with that figure for a moment before reaching that conclusion. £10 million is transformative capital in almost any context. It is enough to eliminate financial anxiety permanently, to fund a serious business venture, to provide housing security for a lifetime, or to build a meaningful investment portfolio that compounds over decades.

The question is never about the number in isolation — it is about what the recipient chooses to do with it. That is the variable I cannot control. What I can control is providing a platform that is genuinely generous and genuinely real. What happens next is up to each individual.

On Gambling and Taking Chances

Discipline over speculation.

Cryptocurrency trading is undeniably volatile — often compared to the Wild West for its absence of regulation and the prevalence of bad actors. That comparison is not entirely unfair. I have seen fortunes built and destroyed in the space of a single quarter. I have watched brilliant people lose everything to overconfidence, and cautious people miss extraordinary opportunities through excessive hesitation.

For those who approach it with genuine discipline, deep research, and the psychological resilience to hold conviction under pressure, the potential is real. My hope is that this gift serves as both cushion and launchpad — providing security while also creating the freedom to back yourself when the right opportunity presents itself. The capital is there. The question, as always, is what you will do with it.

Dreaming Beyond Today

The capital is in your hands.

Whether you are dreaming of the larger house with the boat and the pool, thinking seriously about finally acquiring the restaurant you have managed so well — now that it is available — or simply feel that £20 million sounds considerably more comfortable than £10 million: the capital is in your hands. It can be the beginning of something far bigger.

But this point needs to be made clearly: what you should not expect is for me to have absorbed every risk, every loss, every sleepless night of three decades, only to then be expected to distribute the rewards without any corresponding involvement from the people receiving them. If you want to climb further, you have the capital to do so. The cost of real wealth is not money — it is risk, and the willingness to carry it.

Family Potential — Another Nik

Perhaps there is another way.

If I knew then what I know now, I am not sure I would have taken the same path. The personal cost was extraordinary — higher than I would wish on anyone I care about. I was convicted and sent to prison three times. I did not learn after the second. I had a blatant disregard for financial law and no hesitation in breaking it — not because I was unaware of the consequences, but because I had decided that getting to where I needed to go mattered more than anything else. That arrogance caused real damage to real people. It is not something I am proud of.

When I look at this family now, I do not see those same tendencies — and perhaps that is not a loss. Perhaps it is possible to build something genuinely significant, play with integrity, treat people with fairness, and still arrive somewhere extraordinary. That would be a far better story than mine. I would welcome it.

The Personal Cost

The boundary is clear.

As I put this chapter to rest, I want to be direct about something: it would not be appropriate to ask me for financial assistance beyond what is already provided in this letter. The journey that produced this outcome came at a cost that most people will never fully see — years of relentless work, emotional depletion, physical risk, and the kind of sustained psychological pressure that leaves marks that do not fully heal.

Given the limited support — emotional, practical, or financial — from siblings over the past four decades, and from the younger generation over the past decade, I feel it is both fair and necessary to establish this boundary clearly. This is not resentment. It is honesty. The gifts in this letter are substantial — more than most people in the world will ever receive from anyone. What comes after that is your own to build.

"Risk and reward go hand in hand. If you try to eliminate all risk, you eliminate all reward. The entire business world — and life in general — runs on this balance."

Retirement, Wealth, and Stress

Preserving sanity as much as capital.

The gifts in this letter were carefully structured with a specific purpose: to reduce future financial requests and establish boundaries that are clear, healthy, and sustainable. But substantial wealth brings its own complications. It tends to attract a steady stream of investment pitches, lending requests, and well-meaning suggestions from people who suddenly find themselves interested in what you are doing.

I have no desire to revisit that chapter from the opposite direction. That is why I chose to place my wealth under independent, arm's-length management. The structure covers my living costs, maintains the assets, and protects the remainder. It is not just about preserving money — it is about preserving sanity, and staying honest about my own compulsive tendencies when it comes to high-risk decisions.

Managing the Pool of Funds

You are either in, or you are out.

Significant wealth brings a question that is more subtle than it first appears: who is entitled to enjoy its benefits, and on what basis? If someone declines participation in the Gilding Trust, can they reasonably expect to use the Villa Las Tronas or book time on one of the superyachts? These assets were acquired from the same capital pool that the Trust governs. The answer has to be no — and not out of punishiveness, but out of logic. The benefits and the structure are inseparable. You cannot accept the privileges while declining the framework that makes them possible.

As I have said before in other contexts: you are either in, or you are out. Both choices are valid. Neither is reversible.

Contingency Fund Clause

Unanimity required. No exceptions.

An undisclosed contingency fund has been established. Its balance is not revealed in this letter — and will not be revealed. It exists exclusively for genuine emergencies, and may only be accessed if every beneficiary agrees unanimously.

If a request is approved, the beneficiary who initiated it must understand what they have done: they have drawn on a resource that belonged to the whole family. That decision marks itself. I know this path from personal experience. In my early days, £1 million was never enough — I pressed for more, and lost far more than I had gained. Multiply that lesson by a hundred, add thirty years of compounding mistakes, and you begin to understand why this clause exists and why it is written the way it is.

The fund is there if the family genuinely needs it. It requires unanimity precisely because the decision affects everyone. Without that agreement, the request ends.

Funding a Venture from the Grandchildren's Pool

My capital is locked. Yours is not — but it has rules.

From time to time, one of you may arrive at a moment that feels decisive: a restaurant becomes available, a property comes onto the market, a venture presents itself that seems too compelling to let pass. The first instinct, almost always, is to ask whether I will write the cheque. The answer is settled, and it does not change: my capital is locked, on-chain and by deed, and is not accessible to anyone — not even to me. That door does not open.

There is, however, a structured path through the grandchildren's pool itself. It is not a loan from me. It is a decision the ten of you make together, drawing on the very capital that produces your monthly income — and it carries a cost that every one of you will feel for the rest of your lives. That is by design.

How it works

The £30,000,000 income pool generates your £10,000 monthly payments at a 4% net yield. Withdrawing capital from that pool reduces the yield, and therefore reduces every beneficiary's monthly income — pro rata, equally, for life.

Any request to deploy capital from the pool requires the unanimous written consent of all ten beneficiaries. One refusal ends the matter. There is no appeal, no second vote, no override.

The maximum drawable in a single venture is £10,000,000. The monthly payment may never fall below £5,000 per person per month. This is the structural floor — written into the deed, beyond the reach of any vote, including a unanimous one.

If the venture fails, no one is restored. You will still receive your monthly income — at its new, permanently lower level — for the remainder of your life until age seventy-five. That is the lesson, and the safeguard.

Interactive · Pull the slider

Venture Funding Calculator

Imagine one of you has identified a project — a restaurant, a property, a business. Adjust the slider to model the cost to the entire family if the ten of you agreed unanimously to deploy the capital from your shared income pool.

Capital Requested

£0

£0£2.5M£5M£7.5M£10M

Remaining Income Pool

£30,000,000

Unchanged · full capital intact

Annual Yield Generated

£1,200,000

At 4% net · funds all monthly payments

New Monthly Income · Each Beneficiary

£10,000

No reduction

Annual Income · Each Beneficiary

£120,000

For life · until age 75

FAMILY POSITION

Move the slider to see the cost to each beneficiary of funding a venture from the shared pool.

Conditions of Release

Unanimous written consent of all ten beneficiaries, witnessed and lodged with the Trustees.

A formal business plan reviewed by the Trust's appointed advisors — not as a veto, but as a record.

Capital deployed directly to the venture vehicle. No funds pass through the requesting beneficiary's personal accounts.

The reduction in monthly income takes effect immediately and is permanent. There is no clawback mechanism if the venture succeeds.

The £5,000 monthly floor per beneficiary is absolute and cannot be overridden — not even by unanimous vote.

"If the project succeeds, none of you needed me. If it fails, all of you will have learned — together, with full agreement, and with a monthly income that will still arrive every month for the rest of your life. That floor is not a kindness. It is the lesson, paid forward."

This clause exists because I have funded pet projects before. I have watched what happens when capital is easy to come by and consequences are absorbed by someone else. The structure here is designed to make capital available — but only at a cost that every voting beneficiary will personally and permanently carry. If a venture is genuinely compelling, ten reasonable people will see it. If it is not, the refusal of even one of you is the answer. That is the entire point.

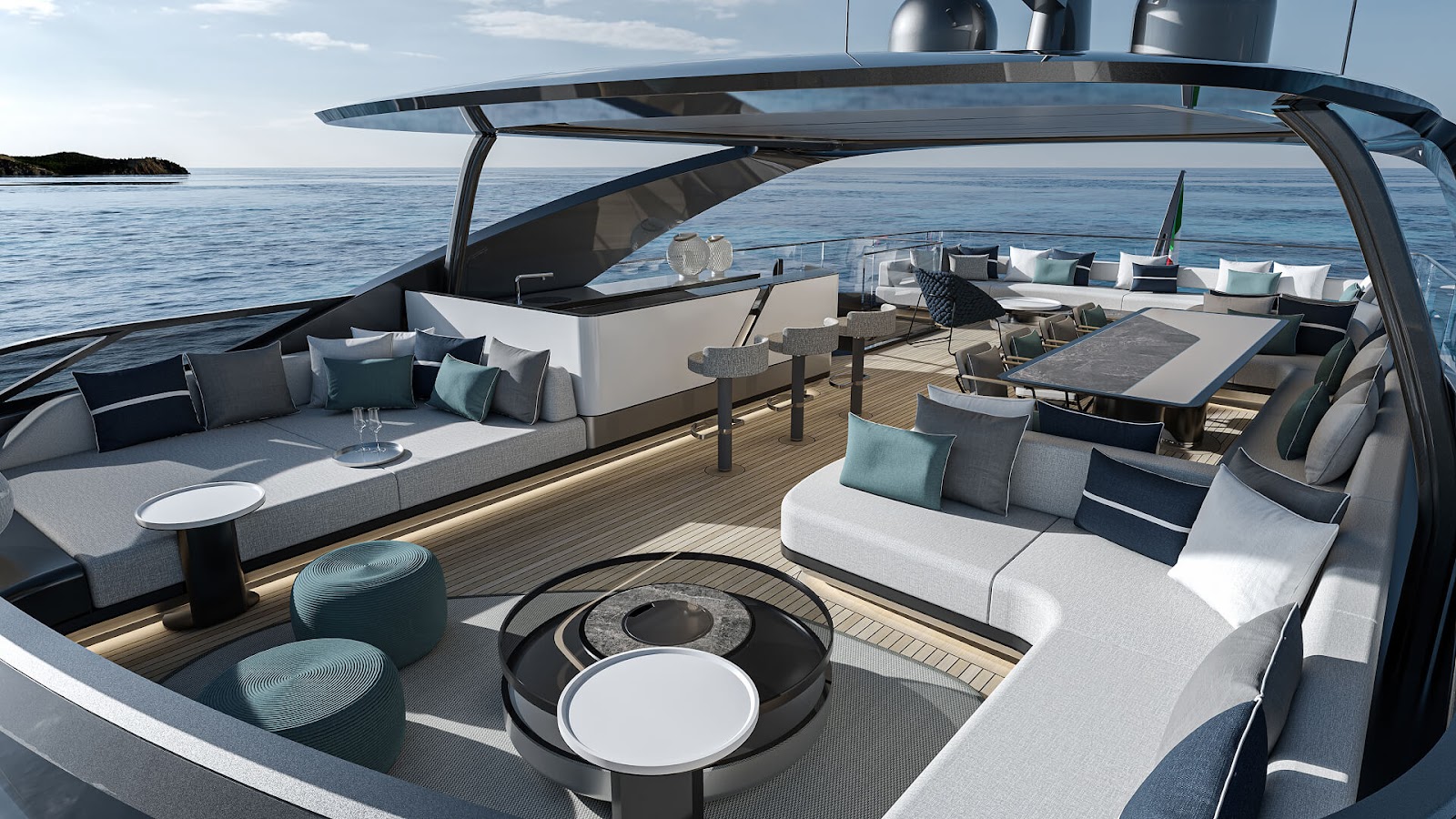

Flagship Holdings

Three assets. One vision.

These three assets were not chosen at random. The superyachts represent the freedom I was always working toward — the open sea, on your own terms. The hotel is the Sardinian coast that kept me going in the dark years, when I watched those videos to remind myself what I was building toward.

🏨 Villa Las Tronas Hotel & Spa

€20,000,000

Built in 1880 by Alessandro, the third Count of Sant'Elia, and later a favourite retreat of the Italian Royal Family until the 1940s — Villa Las Tronas is one of the most singular private estates in Italy, its ancient walls reaching directly to the sea. Perched on its own rocky promontory between Cala Lavatoio and Cala Capone, surrounded on three sides by the crystalline waters of Alghero's gulf — named by many the most beautiful in the Mediterranean.

A five-star hotel of just 25 individually appointed rooms and suites. Indoor heated seawater pool, sauna, hammam, full wellness programme. Panoramic restaurant with strictly seasonal Sardinian cuisine. Private harbour and helipad. Guests have included Antoine de Saint-Exupéry, Liz Taylor, and Richard Burton.

🛥️ ISA Sportiva 43.6M Superyacht

€25,000,000

A masterpiece of Italian craftsmanship — a 43-metre sports yacht where the coupé lines of the automotive world meet the open sea. Designed by Marco Casali with a signature ISA arch connecting the decks. Five staterooms including a full-beam owner's suite, upper-deck saloon converting to private cinema, beach club with fold-down balcony, three sun-pad areas, and a glass-bottomed bow pool.

Twin MTU engines. Top speed 19 knots. Range 3,800 nautical miles — from the Balearics to the Bosphorus without stopping.

DELIVERY: MAY 2028

🚤 ISA Gran Turismo 70M Superyacht

€78,000,000

ISA Yachts' flagship Gran Turismo 70 — 70 metres of coupé-like elegance. Designed by Enrico Gobbi of Team for Design. Steel-grey hull with charcoal detailing and the signature ISA arch. The owner's "glasshouse" suite forward on the upper deck is framed by floor-to-ceiling windows. Five double guest cabins, beach club, spa, and three fold-out swim platforms.

Twin MTU engines. Top speed 17.5 knots. Range 5,500 nautical miles — the entire Mediterranean and beyond, without refuelling.

DELIVERY: Q2 2029

Usage Policies & Privileges

Reserved for Trust beneficiaries.

🏨 Villa Las Tronas

Access 60 days per year — off-season or summer

Eligibility Immediate family & registered partners only

Inclusions Full accommodation, gourmet meals, unlimited spa, business class flights, £1,000 shopping allowance per person per day

Notice Required Minimum 3 months

Cost Completely free under Trust rights

⚓ ISA Superyachts

Access 60 days per year combined across both vessels

Eligibility Immediate family & registered partners only

Inclusions Full crew, all meals & premium wines, fuel, docking fees, business class flights, £1,000 shopping allowance per person per day

For those outside the Trust — a rare opportunity to experience the lifestyle reserved for a select few.

43.6M · Sports Yacht

ISA Sportiva

€125,000/week

Standard rate: €185,000/week

SAVE €60,000

Agile, sleek, and built for those who value speed and style. The Aegean, the Riviera, the Balearics — in a sports yacht that turns heads in every port.

70M · Flagship Superyacht

ISA Gran Turismo

€350,000/week

Standard rate: €500,000/week

SAVE €150,000

The pinnacle of maritime grandeur. 70 metres, twelve guests, a glasshouse owner's suite, beach club, spa, and a range that reaches the Caribbean.

Why Guests Are Required to Pay

Joining after the climb is not the same.

People see the yacht and the calm, not the road that paid for it. My path wasn't funded by banks or family — it was built on pressure, risk, and the resilience that appears only after every polite door has slammed shut.

When legitimate capital refused to back me, I still had companies to build and deadlines that didn't care. So I turned to the only lenders willing to take a chance. I didn't borrow for vice — I borrowed to build, and I repaid every loan, often at interest rates that felt like a survival tax.

A government survey in 2017 found that 11.2% of Italy's micro-businesses relied on extortionate lenders just to stay alive, while nearly 34% collapsed under extreme interest rates. Yet banks still refuse to lend — leaving entrepreneurs with no choice but parallel systems.

Some who backed me early could fill a Netflix crime documentary on organised crime, but without them none of this would exist. That history is why guests contribute when they stay aboard. Not because I need the funds, but because the journey that built this life wasn't free. Close family friends can receive a reduced daily rate of £2,000, paid in fiat or crypto, with a refundable £20,000 security deposit.

"This isn't exclusion — it's acknowledging the real cost of the road that got me here."

If One of You Should Decline

Nothing is lost to the family.

Some of you may decline. I have made my peace with that. Perhaps it will be principle, perhaps pride, perhaps a passing moment of stubbornness that feels larger at the time than it really is. The reason is yours alone, and the choice is yours alone — made freely, without pressure from me or from anyone else.

But let me be plain about what happens next, because it is simpler — and kinder — than the arrangement it replaces. There will be no funds locked away in some vault marked for a rainy day; no waiting for wiser judgement to arrive; no guardian deciding when you are finally ready. That whole apparatus is gone. In its place stands one clean rule:

When a grandchild declines:

Whatever that grandchild would have received — the £10,000,000 and the £10,000 monthly income — is divided equally among the grandchildren who accept

Nothing is held back, nothing is set aside for a later day, nothing is quietly reabsorbed into the vault

The declined share simply passes to those who said yes — and the more who decline, the greater the share for those who remain

Let me be clear about the one door that does not reopen. Once you decline, the Trust is closed to you — finally, and by my hand. I will not reopen it, and the deed will not reopen it for you. If, somewhere down the road, a grandchild who once declined has a genuine change of heart, there is exactly one path left, and only one: to go, cap in hand, to the grandchildren who said yes, and to ask them — gently, and in good faith — "Might I have my share now, please?" The answer might be a warm and immediate yes. It might equally be: "I'm sorry — you made your choice." Both replies are entirely theirs to give, not mine. That is the risk one carries in walking away from a thing freely offered: it does not sit waiting for you; it has already passed to those who stayed.

And here is the part I rather enjoy. Even a grandchild who declines every last penny will find it almost impossible to escape my generosity altogether. There will be birthdays and Christmases, weddings and christenings, summers on the water and winters somewhere warm. There will be presents bought and dinners hosted, holidays shared and a thousand small kindnesses passing between cousins who love one another. The money moves through this family whether you take it directly or not — so the one who declines still, quietly, dines at the same table my success laid out.

The only way to truly miss out would be to refuse the gift and refuse the family — to stop showing up, stop sharing, stop being part of it all. And really — how silly would one have to be to manage that?

"You may decline my money if you wish. You will find it remarkably hard to decline my success — it has a way of reaching everyone at the table, one present, one holiday, one shared evening at a time."

Risks and Rewards

The cost of real wealth is not money.

It is risk, and the willingness to carry it. I scraped together €29,000, lost it all. Rebuilt, lost €740,000. Watched €4.8 million evaporate. Each time, I came back. Not because I was fearless, but because I had nothing else. The work was all I had. And then one day, the pieces connected. I made more in the following four years than in the entire three decades before.

"Risk and reward go hand in hand. If you try to eliminate all risk, you eliminate all reward. The entire business world — and life in general — runs on this balance."

Prosperity for Future Generations

The vault is locked. Literally, on-chain.

Participation in the Gilding Family Trust is voluntary. Anyone may decline, but such a decision is final and irrevocable. Descendants of those who opt out will not be eligible for inclusion.

It is not accessible — not to anyone, not even to me. The assets are bound in smart contracts that cannot be reversed or appealed. Once declined, that path is gone forever.

"Let this be a moment to think not only of what you receive today, but of the legacy you leave tomorrow. The Trust exists to protect, to provide, and to preserve — so that our family's story is one of strength, unity, and opportunity, long after we are gone."

A Path Exists — But It Must Be Earned

Build a billion. The challenge is open.

There is a path forward for anyone in this family who genuinely desires greater wealth. It is the same path I took: build a billion. Honestly, compliantly, through fully verifiable entrepreneurial success — without inheritance, without artificial assistance. Real decision-making authority. Real risk. Real consequence.

If that standard is met, the outcome is:

Appointment as Financial Steward of the Trust

Oversight of all financial and investment affairs

A one-time payout of £100,000,000 to each sibling and every living grandchild

"This is not a gift. It is a challenge — the same challenge life handed to me. The journey is brutal. But it is possible. I proved it."

"Managed with discipline, this sum will sustain our family across generations. But this moment is about more than a number. It is proof that consistency, self-education, and the refusal to quit can take a person further than almost any other combination of advantages. I did not inherit this. I built it."

Nikolas G

Founder, Bitcoin Storm · May 2026 · Confidential — For Family